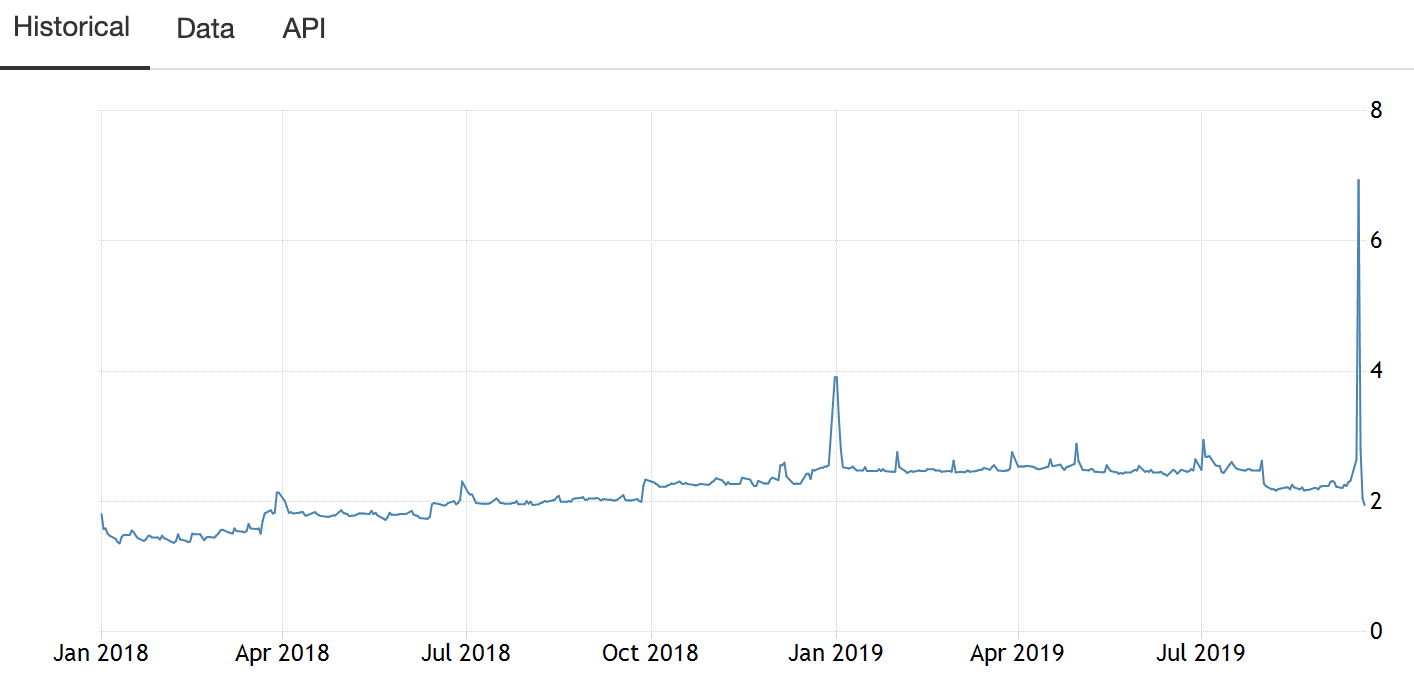

Earlier this week the FED Reserve has to inject additional money into the market to prevent interest rates in money markets overnight loans to shoot up. Last Monday and Tuesday, the short term funds of the banks had dried up and the borrowing cost interest rate went as much as 10% which is four times the Fed’s rate. This is the first time it happened since the last financial crisis, does the history repeating itself?

As of Tuesday, the FED added $125 billion in the market, and until Thursday, it had offered a total of $203 billion, but the bleeding didn’t stop, instead, it worsened.

And this Friday, the FED had once again been forced to pump yet another $75 billion into the market and with a further announcement that if necessary, they will continue to conduct a series of overnight and term repurchase agreement or repo agreement just to maintain the rates within the range.

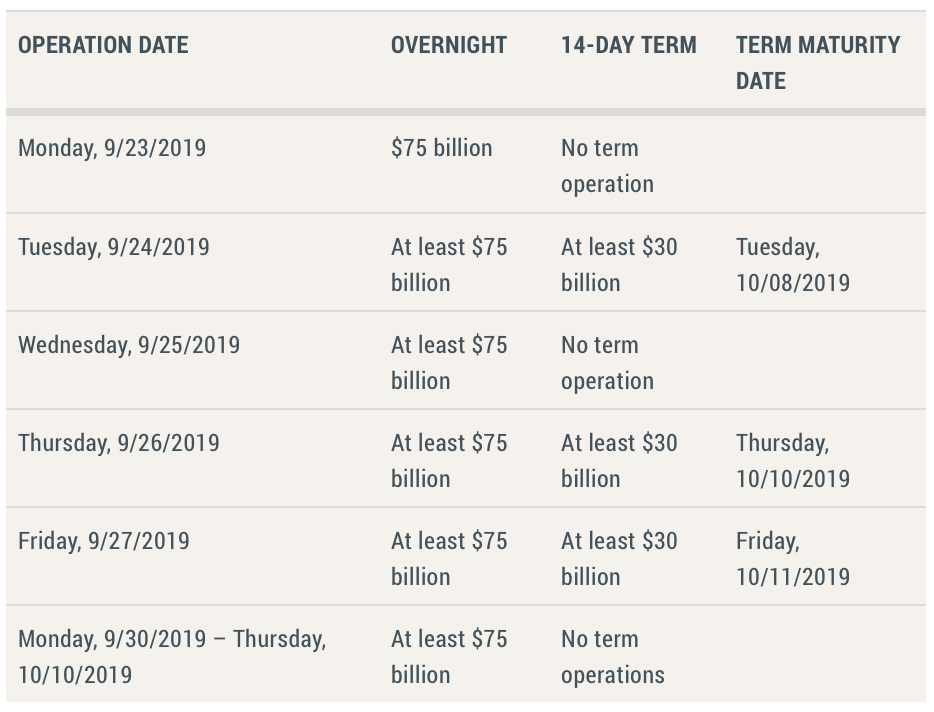

Here is an excerpt of the announcement of the FED Reserve last Sept. 18, 2019:

The Desk will offer three 14-day term repo operations for an aggregate amount of at least $30 billion each, as indicated in the schedule below. The Desk also will offer daily overnight repo operations for an aggregate amount of at least $75 billion each, until Thursday, October 10, 2019.

Below is the Schedule of Overnight and Term Repurchase Agreement Operations extracted from the same announcement:

Before we go any further, let us first discuss what is a Repurchase Agreement or REPO and why is it important.

What is Repo Market?

Repo, which is short for repurchase agreements, are the transactions that amount to short-term loans mostly overnight. It is where the cash and securities met.

In Repo, the firms and banks offer US treasuries and other securities as collateral in exchange of cash. This cash will then be used to finance their trade and lending activities. The next day, these borrowers will pay the loan with additional rate. This rate normally should be close to the FED’s benchmark which is now at 1.75% to 2%. It went down Wednesday by a quarter-point from 2% to %2.25.

Why is it important to maintain the rates within the range?

The repo market stabilizes the U.S. financial system by making sure that the banks are liquid enough to meet its daily requirements including its daily reserves.

Last Tuesday night, the overnight loans interest rates surged to 10% which is four times higher than the FED’s benchmark. The FED is avoiding this to happen because it will disrupt the bond markets and thus affect the overall lending system. The high-interest rates will make trading of stocks and bonds difficult and if it went longer than expected, it could slow the US economy which relies heavily on credit.

What could have caused the bank funds to dry up last Tuesday?

There are a few possible reasons but mostly agree on two things.

- The corporation needed funds for their quarterly bills and withdrawn the same to pay their dues

- The same day, the banks and investors who bought $78 billion notes had to be settled

- The bank reserves are at its lowest since 2011

But what caused for the bank reserves to drop?

After the financial crisis, the interest rates dropped down to almost zero and when it bought more than #3.5 trillion bonds, the banks built up its reserves held at the Fed which peaked at almost $2.8 trillion. But that started to deplete when the Fed started raising its interest rate in 2015, it even went lower when the Fed cut down its bonds in half two years ago.

Last year, they stopped raising the rates and even lowered it in July and then this Wednesday by another quarter-point.

What can the Feds do?

- Provide cash into the market – This is what the Feds did this past three days, from Tuesday to Friday when they injected a total of %228 billion into the money market to normalize the interest rates.

- Lower the interest rates the Fed is paying for the excess reserves – By doing so, the banks may think of lending each other. They did it by lowering the interest rates to 1.8% from 2.1%

- Increase the buying of treasuries and thereby increasing the supply of reserves – By increasing the securities, the Fed also replenishes the bank reserves. It can be tricky though because when you don’t communicate it well, others may think of it as quantitative easing and not as a technical adjustment.

- The Fed is also considering to introduce a new tool called the standing overnight Repo Facility – A permanent financing program allowing participants to exchange their bonds for cash.

{kind=link}

{kind=link}

{kind=link}

{kind=link}